Photo courtesy of Geargodz from Freepik

The Philippines remains heavily reliant on cash despite available electronic payment (e-payments) options. Filipinos still prefer over-the-counter (OTC) transactions for bills payments and cash on delivery (COD) for online shopping. Come the COVID-19 pandemic, regulations, and policies pushed the public to use cashless payments to mitigate risks and ensure public safety.

This is evident according to BSP Governor Benjamin Diokno’s statement that the pandemic has greatly boosted the need for e-payments with banks and other e-payment service providers introducing more innovations to the public. This allowed the growth of digital payments in the Philippines, increasing by 66%. This current trend takes us a step closer to improve financial inclusion in the country.

The Role of E-Payments in Financial Inclusion

Photo courtesy of Thannaree from Freepik

Digital payments and financial inclusion work hand in hand. The continued growth of digital payments provides us an opportunity to improve financial inclusion in the country. While majority of Filipinos still don’t have an account, all of us engage in payments. It can encourage people to open an account to get access to digital and mobile payments as an alternative to cash transactions. However, e-payments aren’t just limited to paying bills and online shopping:

1. Conduct electronic fund transfers (EFT): marginalized Filipinos such as farmers, fisherfolk, MSMEs, and those living on day-to-day paycheck can receive salaries, pension, social security benefits, and government financial assistance safely and more quickly.

2. Expand market reach: allows microentrepreneurs to serve and reach more customers if they provide digital payments in their businesses.

3. Build transaction histories: the use of e-payments helps Filipinos and small businesses to have transaction histories that can support access to other financial services such as credit.

4. Encourage the use of other financial services: as more people get used to online payments, they can eventually apply for savings, investments, loans, and insurance.

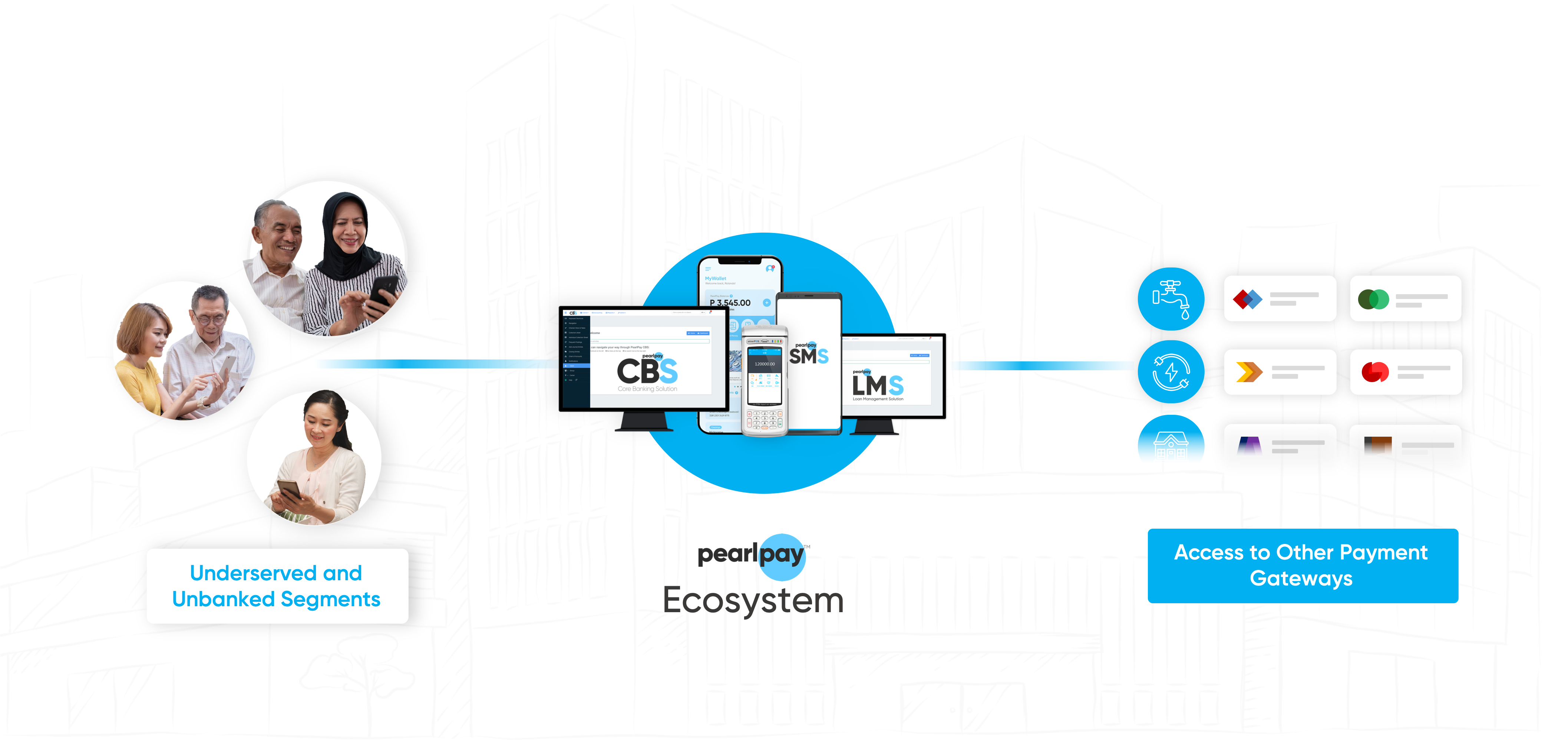

Helping Institutions Connect to Payment Gateways

Photo courtesy of Skawee from Freepik

The Bangko Sentral ng Pilipinas (BSP) reported during their Ulat sa Bayan event last February 19 that the volume of PESONet transactions surged to 15.3 million while InstaPay payment reached 86.7 million in 2020. The growth of digital payments emphasized the need to improve digitalization in the Philippines. The 38.88 million Filipinos transacting digitally highlights the need for more institutions to connect to payment gateways to meet the needs of the public. But how can they do that?

Financial institutions can partner with Fintech providers that can equip them with the proper foundation for their transformation. They can seamlessly integrate other solutions, such as mobile banking, to make it easier for customers to access digital payments. They can have an interconnected payment system to ensure safer and secure cashless transactions for Filipinos.

More than that, institutions can also provide accessible financial resources to their communities. Low-income families, MSMEs, and the agricultural sector have been affected heavily. The economic impact has resulted in the loss of jobs, income, and small businesses to close down. Digitalization will not just help people recover from the pandemic but also provide them the means to grow in the long run.

Related Posts

Digital Transformation for Financial Institutions: Unleashing Their Potential With the Right Foundation

Understanding how to set up the right foundation for digital transformation can empower financial…

Unlocking Business Opportunities in the Philippines Through Payment Gateways

Read how connecting financial institutions to payment gateways in the Philippines can provide…

Benefits of Digital Transformation: Encouraging the Growth of Financial Institutions and Communities in the Philippines

Learn more how digital transformation in the Philippines can benefit rural banks and encourage…